Example of Full Price Payment and Seller Financing in a Land Contract

When selling a piece of land, one option available to sellers is financing the sale themselves. Seller financing can offer significant tax benefits compared to receiving the full purchase price upfront. This blog post will explore an example of seller financing in a land contract, highlighting how it can reduce the seller's tax liability and provide flexibility to the buyer.

As we can see above, John's tax bracket jumped from 22% to 32% when it is a full payment. However, with seller finance, not only John's tax bracket stays only between 22% - 24%, he also receives 10% interest rate. At the end, with seller finance, John actually gets $50,000 + $250,000 + $156,452 (Interest on remain $250,000) + $37,750 (Tax Saving) = $494,202. That is 64% more than a traditional sell of $300,000.

The following has the detailed calculation.

Scenario:

Seller: John owns a piece of land valued at $300,000.

Buyer: Jane wants to purchase the land but only has $50,000 available.

Seller Financing Agreement: John agrees to finance the remaining $250,000 over 10 years at a 10% interest rate.

Full Price Payment Scenario:

Purchase Price: $300,000

Down Payment: $300,000 (Jane pays the full amount upfront)

Seller's Cost Basis: $150,000

Capital Gain: $150,000

Tax Impact on Seller (Full Price Payment):

Capital Gains Tax:

John must pay taxes on the entire $150,000 capital gain in the year of the sale.

Assuming a capital gains tax rate of 20%:

Tax Owed: $150,000 * 20% = $30,000

Higher Tax Bracket:

The full $150,000 gain is added to John's income for the year, potentially pushing him into a higher tax bracket, from 22% to 32%.

This could result in a higher overall tax liability for the year.

Seller Financing Scenario (10% Interest Rate):

Purchase Price: $300,000

Down Payment: $50,000

Financed Amount: $250,000

Interest Rate: 10%

Loan Term: 10 years

Annual Payment: $40,465

Tax Impact on Seller (Seller Financing):

Tax Deferral:

John defers capital gains taxes, paying incrementally as he receives payments.

For simplicity, let's assume the first year's principal portion is $15,465 and interest is $25,000.

Taxable Gain (Principal Portion): $15,465 * 50% = $7,732.50

Capital Gains Tax (20%): $7,732.50 * 20% = $1,546.50

Lower Tax Bracket:

By spreading the income over several years, John may avoid moving into a higher tax bracket.

This reduces his overall tax liability compared to a lump sum payment.

Total Tax Impact Over 10 Years:

Assuming the principal repayment and taxable gain are consistent over the 10 years:

Total Taxable Gain: $150,000

Total Capital Gains Tax (20%): $150,000 * 20% = $30,000

Note: Tax is paid incrementally, which could potentially reduce the total amount due to remaining in a lower tax bracket each year.

Comparison:

Full Price Payment:

Immediate Cash: $300,000

Total Tax Paid: $30,000 (20% of $150,000 gain)

Higher Tax Bracket: Possible due to the large gain in one year.

Seller Financing (10% Interest Rate):

Immediate Cash: $50,000 (down payment)

Annual Payments: $40,465

First Year Tax Liability: $1,546.50 (20% of $7,732.50 gain)

Interest Income: $25,000 in the first year

Lower Tax Bracket: Likely, due to spreading the gain over multiple years.

Total Tax Paid Over 10 Years: $30,000 (20% of $150,000 gain)

Tax Calculation for Full Price Payment Scenario:

Total Income: $250,000

Calculate Taxes for Standard Income ($100,000):

10% on the first $11,000: $1,100

12% on the next $33,725: $4,047

22% on the next $50,650: $11,143

24% on the remaining $4,625: $1,110

Total Tax on $100,000: $1,100 + $4,047 + $11,143 + $1,110 = $17,400

Calculate Taxes on Additional Income ($150,000):

24% on the next $81,725: $19,614

32% on the remaining $68,275: $21,848

Total Tax on $150,000: $19,614 + $21,848 = $41,462

Total Tax:

$17,400 + $41,462 = $58,862

Tax Calculation for Seller Financing Scenario (First Year):

Total First Year Income: $115,465

Calculate Taxes for Standard Income ($100,000):

Same as above: $17,400

Calculate Taxes on Additional Income ($15,465):

24% on the remaining $15,465: $3,711.60

Total Tax:

$17,400 + $3,711.60 = $21,111.60

Tax Savings with Seller Financing:

Total Tax Paid in Full Price Payment Scenario: $58,862

Total Tax Paid in Seller Financing Scenario (First Year): $21,111.60

Tax Savings in the First Year: $58,862 - $21,111.60 = $37,750.40

Summary:

Full Price Payment Scenario:

Receives full payment upfront.

Faces a significant tax bill immediately.

Total Tax Paid: $58,862.

Potentially moves into a higher tax bracket.

Seller Financing Scenario (First Year):

Receives a down payment and annual payments.

Defers tax liability, paying incrementally.

Total Tax Paid: $21,111.60.

Likely remains in a lower tax bracket.

Receives additional interest income over the loan term.

Seller financing can provide significant tax savings by spreading the capital gains over several years, keeping the seller in a lower tax bracket and reducing the overall tax liability. This strategy not only benefits the seller but also makes the purchase more accessible for the buyer.

The above example is for educational purpose only. For your own situation and tax saving, please consulate with your own tax advisor.

When selling a piece of land, one option available to sellers is financing the sale themselves. Seller financing can offer significant tax benefits compared to receiving the full purchase price upfront. This blog post will explore an real example of seller financing in a land contract, highlighting how it can reduce the seller's tax liability and provide flexibility to the buyer.

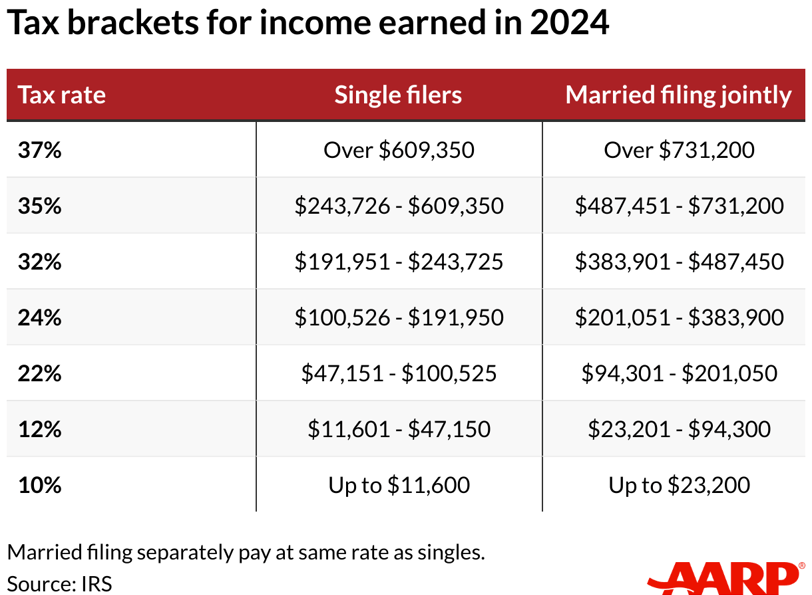

Here we assume Seller John is selling a piece of land he bought years ago with $150,000 as cost and selling for $300,000, which means he has $150,000 as capital gain. We also assume John's other income is $100,000. So if John sells this land and get the full payment, he would need to pay income tax on $250,000. before we go further, let's take a look the latest tax bracket table in 2024, as below: